Hennessy Capital Investment Corp. VII (HVII)

Next Generation SPAC Vehicle for Industrial Tech and Energy Transition Companies Looking to Go Public

- Backed by one of the leading and most experienced SPAC sponsors, Hennessy Capital Investment Corp. VII (HVII) is a blank check company targeting high-growth businesses in industrial technology and energy transition, two sectors undergoing transformative tailwinds fueled by decarbonization, digitization, reshoring, and government incentives. HVII is backed by the Hennessy Capital Group (HCG), which has announced, completed or otherwise served as an advisor to 12 successful SPAC transactions representing $7 billion+ in enterprise value and has consistently helped growth-oriented companies access capital, strengthen operations, and build shareholder value.

- We believe HVII, with $190 million+ in Trust Account, is an ideal SPAC partner for private companies (EV >$500mn) belonging to the above sectors, looking to go public:

- Experienced leadership team with demonstrable success across market cycles. Led by Daniel J. Hennessy, who has 17x SPAC experience, HVII’s team has successfully completed multiple SPAC transactions across diverse industries, including mobility, logistics, and digital infrastructure, in the past decade. This proven ability to attract institutional investors and secure complex deal financing underscores HVII’s appeal as a partner for private companies.

- Proven platform with strong execution history and industry alignment. SPACs sponsored or co-sponsored by HCG have completed multiple successful de-SPAC transactions including Blue Bird, Daseke, LatAm Logistic Properties, and most recently Namib Minerals. Its strategy emphasizes finding targets with strong competitive moats, differentiated technology, scalable growth models, and experienced leadership teams. Past deals illustrate the team’s ability to optimize capital structures, attract strategic partners, and accelerate public readiness of private businesses.

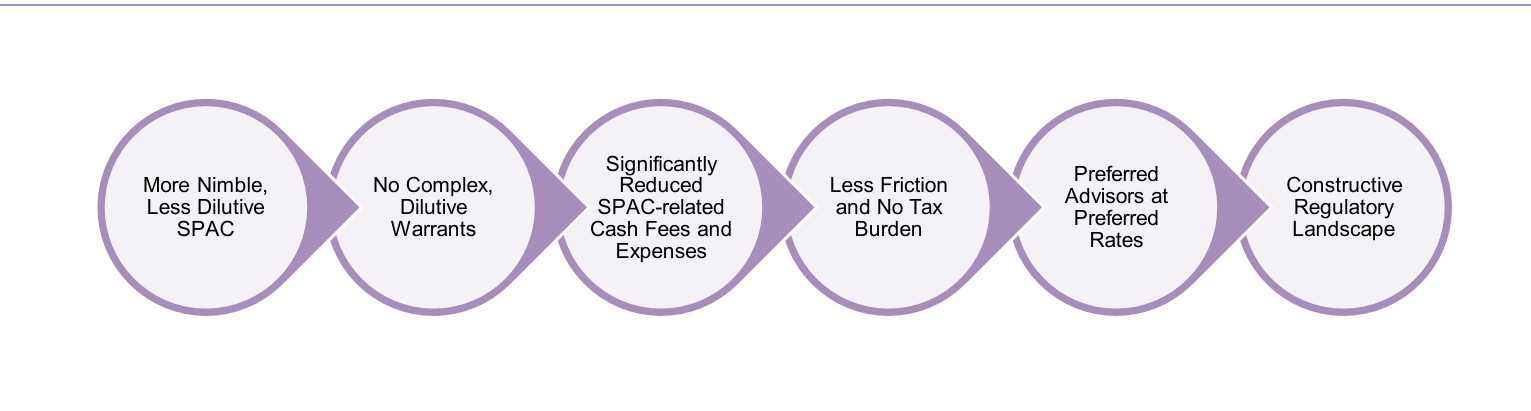

- HVII – Rethinking the SPAC Structure: The Case for Rights over Warrants. HVII stands out with its rights-only approach. Warrants are often misunderstood and mispriced, thus eroding value. Post-merger, they introduce valuation complexity, earnings volatility, and a persistent overhang that suppresses share performance. HVII’s rights-based units (1/12th right per unit) eliminate these issues, offering simplicity, transparency, and reduced dilution risk. We believe HVII’s structure signals a shift toward investor-friendly, sustainable models that are better aligned with target company needs and position the combined company for healthier postmerger stock performance.

- Reduced fees, expenses, and tax burden. Performance-based underwriting fees enables lower transaction cost while Cayman domicile advantage results in efficient cross-border deal execution. HVII has also partnered with leading SPAC advisors at preferred rates. This, coupled with management team’s experience of navigating compliance for a smooth listing, also enhances HVII’s appeal as a SPAC partner for high-growth private companies

Company Overview

HVII – A Cayman Domiciled SPAC With Deep Expertise and a Strong Track Record

- The SPAC offers private companies a compelling and differentiated path to the public markets for companies seeking a successful public listing on Nasdaq. HVII’s flexible capital structure, experienced sponsor team, and alignment with shareholders, positions it as a compelling partner for transformative businesses. HVII offers not just capital, but a proven platform that is optimized to help private companies transition into the public markets with confidence. Beyond the structural efficiency of a SPAC vehicle, HVII brings a strong track record of delivering value through SPAC business combinations, and a focused investment strategy that aligns with transformative sectors such as industrial technology and energy transition. Hennessy Capital Group has announced, completed or otherwise served as an advisor to 12 successful SPAC transactions representing $7 billion+ in enterprise value and has consistently helped growth-oriented companies access capital, strengthen operations, and build shareholder value.

- HVII is designed to effectuate its business combination using cash from the trust, equity, debt, or third-party financings such as PIPEs or loans, with a goal to find a category-winner to bring public in 2025. HVII offers flexibility in structuring transactions, allowing deals to be tailored to the operational, capital, and strategic needs of target companies. While the company has not initiated substantive discussions with targets, it benefits from its management’s network built through prior SPACs like Hennessy VI, helping to surface high-quality opportunities in focus sectors.

- HVII’s investment strategy leverages the expertise of its management and market dynamics. In the current SPAC environment, success is no longer driven by access to capital alone, and today, the most effective SPACs are those with a focused investment strategy. An effective strategy aligns the operational and sectoral expertise of the sponsor team with industries positioned for sustained growth and transformation. For private companies evaluating a SPAC partner, this alignment is crucial, as it directly impacts the SPAC’s ability to identify quality targets, structure transactions thoughtfully, and create long-term shareholder value. HVII exemplifies this approach by zeroing in on industrial technology and energy transition businesses with enterprise values of $500 million or greater. These are the sectors where its management team’s extensive experience provides a decisive advantage.

- The competitive landscape for SPACs has shifted dramatically. The number of active SPACs has declined from 600+ in 2021 to fewer than 100 today (as of June 2025), according to SPAC Insider. At the same time, the pipeline of companies seeking to go public remains strong. According to Dealogic, around 250 companies are actively pursuing a public listing, with many more having confidentially filed. This backlog of companies, combined with the pent-up demand from private equity and venture capital firms facing record holding periods (per Pitchbook) presents HVII with a rich universe of potential partners. HVII’s team has a proven track record of unlocking value for private equity owners, and this was demonstrated in successful transactions like Blue Bird (Hennessy I) and NRC Group (Hennessy III). These partnerships highlight the team’s ability to deliver liquidity and accelerate growth for private equity-backed companies.

- Further strengthening HVII’s investment strategy are macroeconomic tailwinds. U.S. supply chain reshoring, fueled by ~$750 billion in federal programs including CHIPS Act and Inflation Reduction Act, among other, combined with competitive energy costs are driving what HVII describes as an industrial and manufacturing renaissance. By aligning its focus with these transformative trends, HVII positions itself and its potential partners to capitalize on powerful, long-term catalysts for growth.

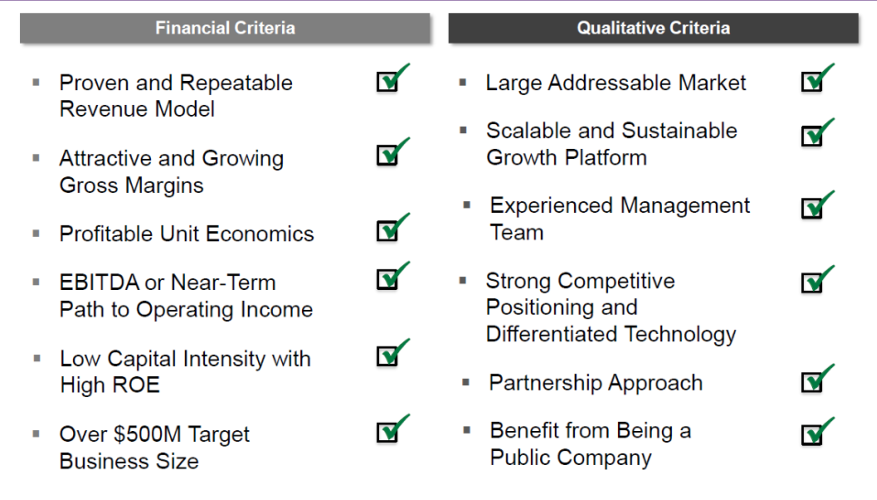

Chart 1: Acquisition Criteria of HVII

- HVII follows a disciplined and strategic acquisition approach focused on identifying high-potential businesses, that align with its strengths and long-term vision. The SPAC seeks targets with an enterprise value of at least $500 million, operating within large, addressable markets tied to industrial technology and the energy transition. HVII prioritizes businesses with scalable, sustainable growth platforms that benefit from megatrends like automation, efficiency, and digital transformation. Ideal candidates will possess strong competitive positioning, defensible intellectual property, and differentiated technology aimed at solving critical industry challenges.

- A key selection factor is the presence of an experienced, capable management team aligned with HVII’s partnership-oriented philosophy. HVII’s leadership team brings deep operating and investing experience and aims to complement the target’s existing capabilities to drive long-term value. Importantly, HVII also favors businesses that can benefit from going public, gaining broader access to capital and increased visibility in public markets.

Management Team

Best-In-Class Team with Demonstrable Success Across Industries and Market Cycles

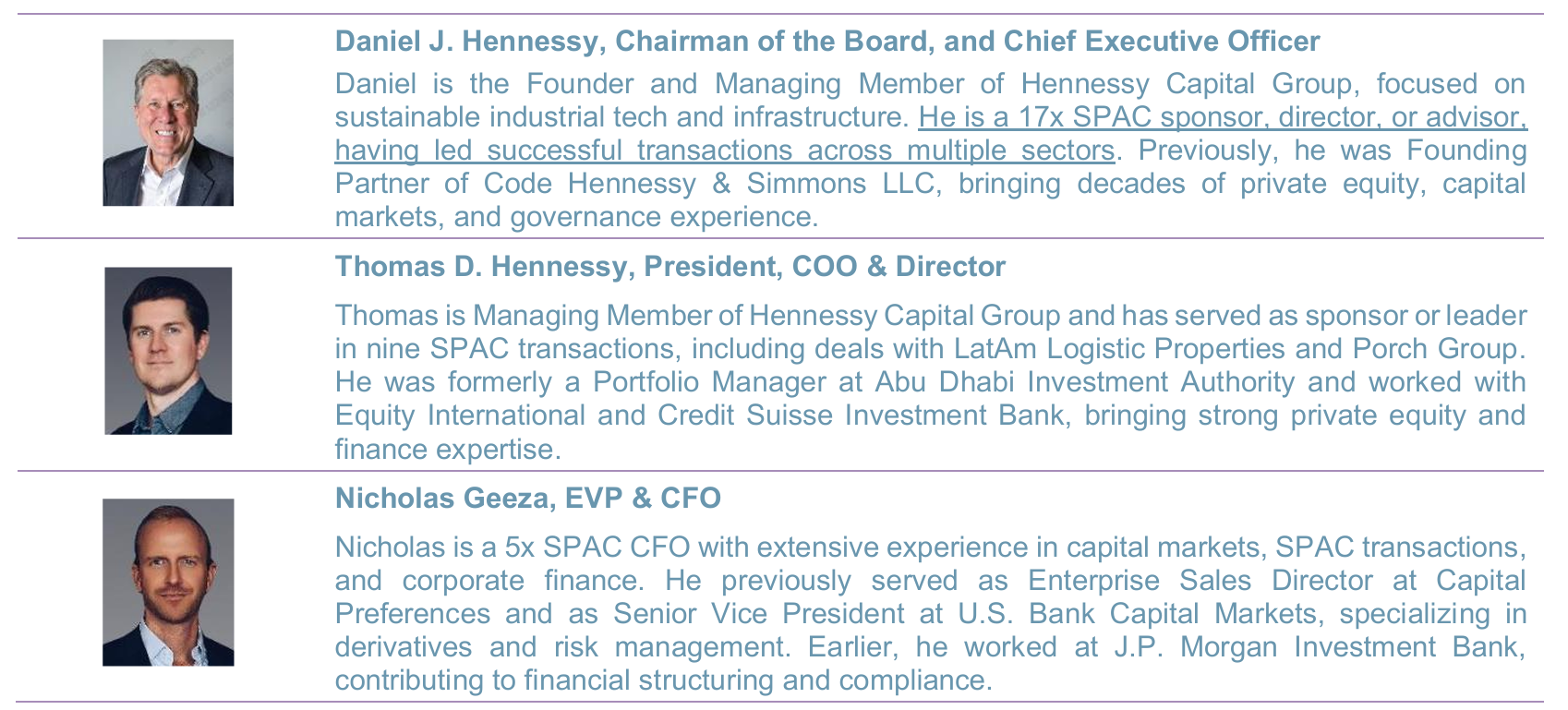

- Led by Daniel J. Hennessy, HVII has a highly experienced and proven investment team, with one of the most consistent and credible track records in the SPAC ecosystem and proven ability to generate value across industries and market cycles. Over more than a decade, Mr. Hennessy has led multiple SPACs, all focused on sectors with long-term value creation potential, including industrial technology, transportation, and energy transition. Notably, business combinations under his leadership, such as with Blue Bird Corporation and Daseke, Inc., have successfully navigated post-merger integration challenges while delivering durable shareholder value. This is a critical differentiator, as many SPAC sponsors lack operational follow-through post-closing. Supporting Daniel is Thomas D. Hennessy, who complements the team with modern sectoral expertise, particularly in technologyenabled infrastructure and smart mobility. His role in SPAC transactions involving companies like Porch Group, Inc. highlights his ability to identify scalable platforms and work collaboratively with founders. Together, the duo brings a rare blend of traditional industrial operating experience and forward-looking innovation focus — exactly the balance target companies seek when choosing a SPAC partner. The team is further strengthened by Nicholas Geeza, a seasoned SPAC CFO who brings strong expertise in financial structuring and risk management and is supported by Megan Cai and Joshua Richardson who bring their investment banking, strategic finance, and financial advisory expertise to the team.

- In addition to operational experience, the HVII team has demonstrated capital markets strength, having repeatedly secured PIPE financing from reputable institutional investors. Their strong institutional relationships enhance credibility and increase the likelihood of a smooth de-SPAC process with adequate funding. Importantly, the team has significant skin in the game, with sponsor capital at risk, and a history of structuring deals with alignment to long-term shareholder interests beyond just closing fees. For private companies evaluating SPAC options, HVII offers the advantage of partnering with a management team that combines sector expertise, capital markets credibility, and a commitment to long-term value creation.

Chart 2: HVII – Management Team

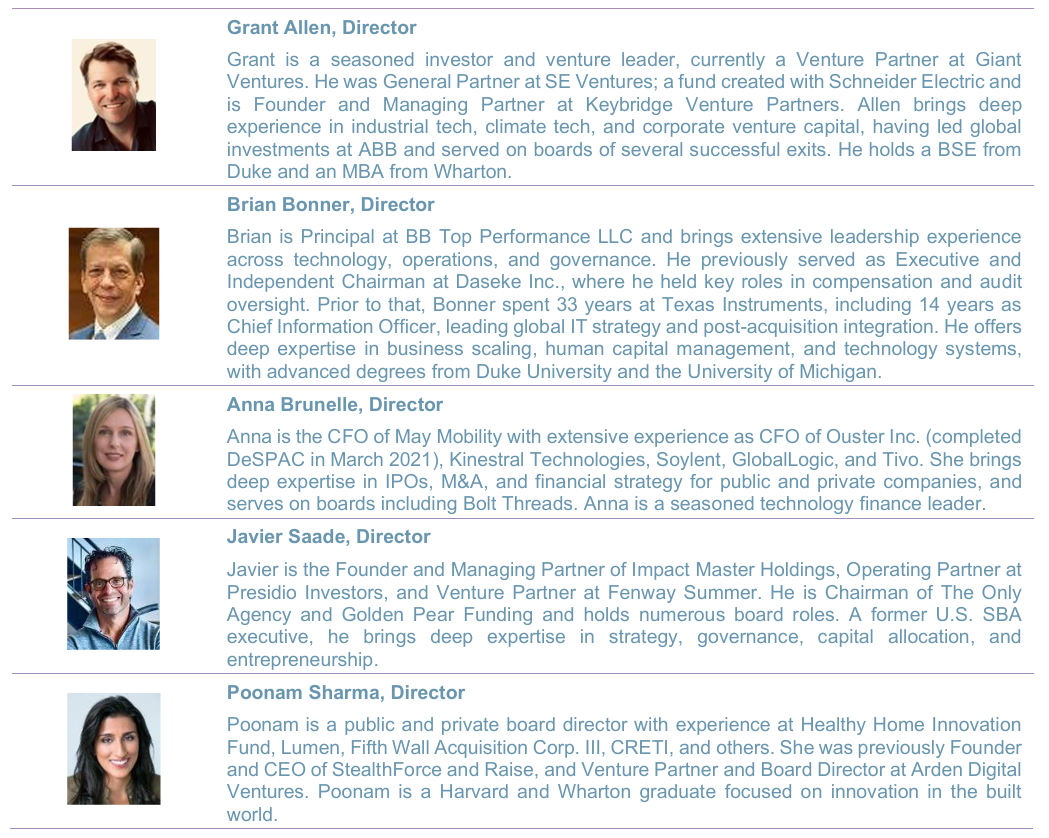

- The management team is supported by a world-class Board of Directors that comprises individuals with diverse and relevant expertise required to drive shareholder value creation. Grant R. Allen offers deep insights from his tenure at ABB and venture capital experience with SE Ventures. Brian Bonner contributes over three decades of leadership from Texas Instruments, focusing on technology and governance. Anna Brunelle brings financial acumen from her CFO roles at May Mobility and Ouster Inc., including navigating SPAC mergers. Javier Saade adds strategic depth with his background in venture capital and public service, including his role at the U.S. Small Business Administration. Poonam Sharma, chair of the audit committee, enhances the board's financial oversight capabilities.

Chart 3: HVII – Board of Directors (in addition to Daniel J. Hennessy and Thomas D. Hennessy)

Exec Edge Research, HVII Investor Presentation

Backed by a Proven SPAC Sponsor with Unmatched Capital Markets Execution Capabilities

- HVII enters the SPAC landscape as a highly credible platform, backed by one of the most experienced and successful SPAC sponsors with a long and successful track record of business combinations around the $500 million range. A SPAC’s ability to deliver value to its target company goes far beyond identifying a promising business — it hinges on its capital markets expertise. The right SPAC partner must skillfully structure transactions, secure institutional investor support, and guide the target through the complex journey of becoming a successful public company. This is where HVII sets itself apart. Backed by the Hennessy Capital Group, one of the most experienced SPAC sponsors globally, HVII’s management has demonstrated unmatched capability in raising, deploying, and managing capital across diverse sectors and geographies. Hennessy Capital Group has announced, completed or otherwise served as an advisor to 12 successful SPAC transactions representing $7 billion+ in enterprise value and has consistently helped growth-oriented companies access capital, strengthen operations, and build shareholder value. This proven ability to attract institutional investors and secure complex deal financing significantly enhances HVII’s appeal as a partner for private companies considering a public listing. The recent business combination of Hennessy VI with Namib Minerals (NAMM), which closed in June 2025, exemplifies this strength — structuring a $602 million enterprise value deal with up to $75 million of net proceeds to fuel Namib’s

Chart 4: Strong Track Record of Closing Business Combinations for More Than 10 Years

Case Studies

Recent Business Combinations of SPACs backed by the Hennessy Capital Group

- HVII belongs to the Hennessy Capital Group (HCG), a proven sponsor and co-sponsor of SPACs across compelling platforms. Below, we discuss some of the recent business combinations across sectors closed by SPACs – two, Hennessy Capital Investment Corp. VI, and Learn CW Investment Corporation – belonging to Hennessy Capital Group in the recent past.

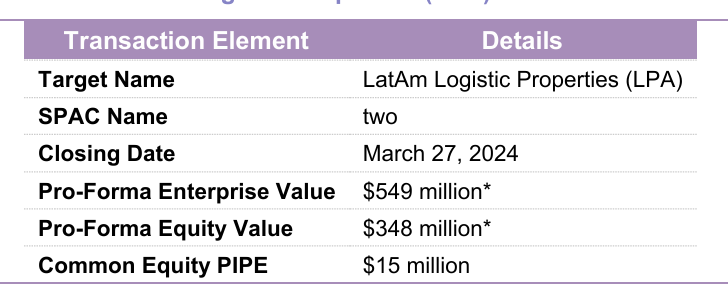

- Transportation: LatAm Logistic Properties (LPA). The business combination between LatAm Logistic Properties (LPA) and the SPAC two (erstwhile TWOA) in March 2024, exemplifies the strengths of HCG’s differentiated SPAC platform: strategic investment focus, management excellence, right-sized transaction structuring, and strong partner networks. LPA, a vertically integrated developer and operator of Class A industrial and logistics properties in Central and South America, reflected the kind of business that aligned closely with two’s investment strategy. The company operates in sectors benefiting from major macroeconomic tailwinds, notably, the surge in e-commerce and reshoring trends that have driven industrial capital values higher. two’s ability to identify such sectoral sweet spots, and its disciplined focus on industrial technology and related infrastructure, enabled it to recognize LPA as a compelling partner. Importantly, the transaction was right sized for success. The pro forma enterprise value of approximately $549 million and equity value of $348 million matched the stated focus on businesses above $500 million in enterprise value ensuring that the capital structure was appropriately balanced to meet the needs of both LPA and public market investors. The inclusion of a $15 million PIPE further highlights HCG’s ability to draw on its partner network to provide supplemental growth capital and enhance transaction certainty.

- The strength of the group’s management and partner network is reflected not only in the structure of the deal but also in the post-merger outlook. LPA’s business model offering multinational tenants institutionalquality facilities with expansion optionality resonates with HCG’s experience in scaling platforms that serve complex, growth-oriented customer bases. Moreover, LPA’s strong financial profile, with unlevered development yields of up to 10% and long-term leases supported by attractive local debt, underscores the kind of disciplined, value-creating business the group aims to bring to public investors.

- LPA ranked among the top 5 DeSPAC’s in 2024 shortlisted by Cohen & Co. based on share price as of 12/31/24. This transaction also demonstrates the SPAC’s ability to partner with accomplished management teams like LPA’s, who bring deep regional expertise and governance experience aligned with international public company standards a critical success factor in cross-border industrial real estate.

Chart 5: Transaction Overview – LatAm Logistic Properties (LPA)

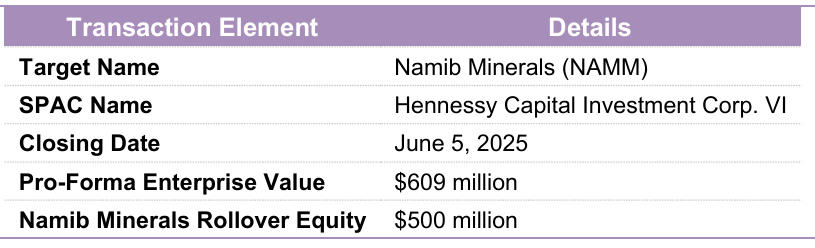

- Mining: Namib Minerals (NAMM). The business combination of Hennessy Capital Investment Corp. VI (erstwhile HCVI) with Namib Minerals (NAMM), which closed in June 2025, is a strong example of how HCG’s leadership applies its proven investment strategy, management expertise, and network strength to identify and structure valueaccretive deals. The transaction, with a pro-forma enterprise value of $609 million and $500 million of rollover equity, is well aligned with the focus on partnering with scaled businesses in high-potential sectors. Namib Minerals represents a Pan-African, multi-asset mining platform with a focus on precious and critical metals. Its portfolio includes three high-grade, low-cost gold mines in Zimbabwe, combining one active mine with two that are being restarted. This strategic footprint, paired with Namib’s long-standing track record in mine development and operations, illustrates the group’s ability to source transactions that combine near-term cash flow with significant growth optionality.

- HCVI’s management team demonstrated its strength by partnering with a company operating in a sector experiencing powerful macro tailwinds, including a global refocus on precious metals and critical minerals supply security. This reflects a disciplined, research-backed approach to sector selection, a key differentiator in a crowded SPAC landscape.

− The rightsizing of the transaction with a valuation comfortably above the $500 million target threshold ensures alignment with both public market investor expectations and Namib Minerals’ growth financing requirements. Further, the deal structure showcases flexibility and the strength of the SPAC’s network in securing a rollover from Namib’s owners, enhancing alignment between the company and its future public shareholders.

− Namib’s financial profile, with estimated EBITDA of $230 million at target production capacity (per HVII’s investor presentation), combined with strong support from the Zimbabwean government (which has committed $364 million toward creating a conducive mining environment) reinforces the attractiveness of this transaction.

Chart 6: Transaction Overview – Namib Minerals (NAMM)

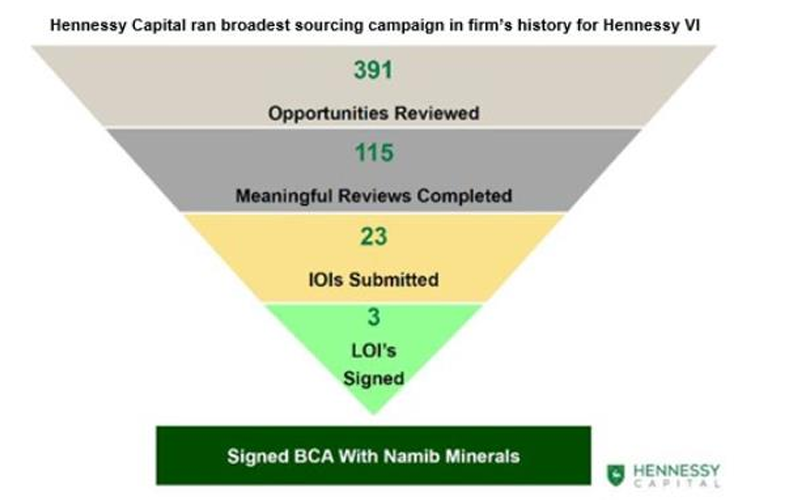

Chart 7: Example of Broad Sourcing Campaign Ran by HCVI for Namib Minerals

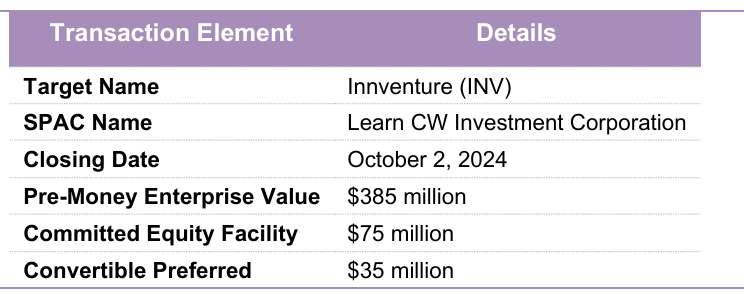

- Industrial Technology Platform: Innventure (INV). The business combination between Innventure and Learn CW Investment Corporation (erstwhile LCW), that closed in October 2024, demonstrates HCG’s disciplined focus on backing transformative, high-potential technology platforms that align with global sustainability trends. The transaction, featuring a pre-money enterprise value of $385 million, along with a $75 million committed equity facility and $35 million in convertible preferred equity, reflects the ability to tailor capital structures to support complex, innovation-driven businesses while maintaining alignment with public market expectations. Innventure operates as a sustainable industrial technology company builder, founded with a mission to identify, fund, and scale breakthrough technologies licensed or acquired from major multinational corporations. With partnerships including Procter & Gamble and Nokia, Innventure provides an excellent example of the Hennessy Capital Group’s strength in leveraging networks to access proprietary, high-value opportunities. Innventure’s differentiated, systematic model for de-risking and scaling disruptive technologies through proprietary market analytics and data-driven processes, speaks to HCG’s philosophy of backing businesses with repeatable, disciplined growth engines. The company’s launch of three businesses (PureCycle, Aeroflexx, and Accelsius) underscores the robustness of this platform and its ability to create meaningful enterprise value, with PureCycle alone achieving a successful Nasdaq listing.

- The transaction structure, which blends traditional equity with committed capital and convertible preferred instruments, reflects flexibility in structuring deals that provide target companies with the capital certainty they need to execute their growth plans. This right-sizing of the transaction combined with the backing of a best-in-class management team, positions Innventure for success as a public company, while ensuring alignment with shareholder interests.

− Innventure also ranked among the top-5 DeSPAC’s in 2024 shortlisted by Cohen & Co. based on share price as of 12/31/24. Its focus on building companies around technologies with $1 billion+ enterprise value potential is a compelling fit for LCW’s goal of delivering high-quality business combinations in sectors where industrial technology, sustainability, and innovation converge.

Chart 8: Transaction Overview – Innventure (INV)

Structured-to-Win

Next-Generation SPAC Vehicle Crafted to Drive Value Creation and Operational Success

- In today’s SPAC market, where credibility, efficiency, and alignment matter more than ever, HVII distinguishes itself through a thoughtfully engineered structure designed to deliver superior outcomes for its merger partner. Unlike many SPACs of the past that followed generic templates, HVII’s offering details reflect a deliberate effort to reduce dilution, lower transaction costs, and streamline execution, while preserving flexibility to support the long-term growth of its target company. From a right-sized IPO that aligns capital raised with the needs of companies valued above $500 million, to a clean, zero-warrant capital structure that eliminates unnecessary overhang, every element of HVII’s design has been crafted to foster value creation and operational success. HVII’s performance-based fee model, Cayman Islands domicile, and engagement of top-tier advisors at efficient rates all reinforce its commitment to being a responsible, high-quality partner. Additionally, the team’s deep regulatory experience ensures that the process of transitioning to the public markets is handled with discipline and transparency. For private companies looking to access public capital, HVII offers a rare combination of structural efficiency, experienced leadership, and strategic alignment, positioning both the SPAC and its merger partner to win in today’s competitive environment. We discuss the Structural elements that position HVII to win, below:

Chart 9: Structural Elements that Set HVII Apart

- A right-sized SPAC structure for efficient growth partnerships. HVII’s $190 million IPO is carefully designed to match today’s market conditions and the needs of high-quality merger targets. Unlike oversized SPACs that often struggle with capital bloat and inefficient deployment, HVII’s right-sized offering is aimed at businesses with enterprise values over $500 million — providing sufficient scale to fund growth without unnecessary dilution. For target companies, this structure offers a streamlined path to access public capital markets while preserving equity value for founders and existing investors. The balance between IPO size and target value ensures that proceeds can be effectively allocated toward expansion, innovation, or debt reduction, rather than excessive redemptions or balance sheet inefficiencies.

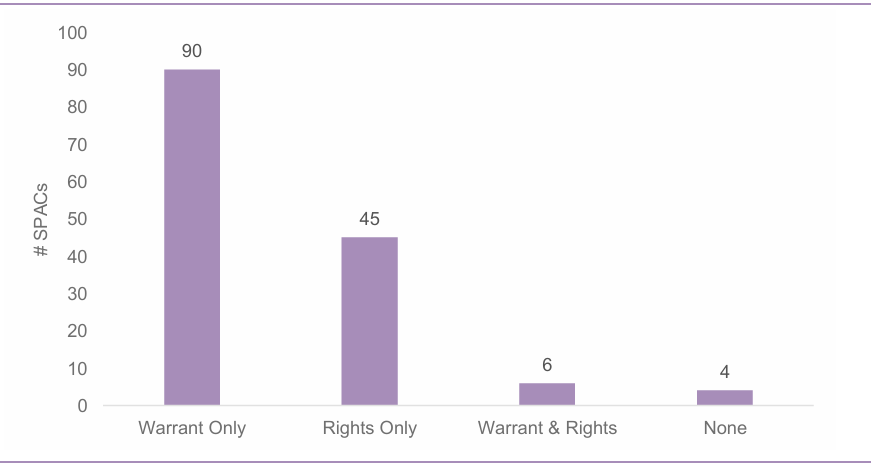

- HVII – Rethinking the SPAC Structure: The Case for Rights over Warrants. The traditional SPAC unit, comprising common shares and fractional warrants, has long dominated the market. As of July 9, 96 out of 145 (66%) of SPACs that are currently searching for a target have a warrant or a warrant + rights structure, per data from SPACInsider.com. Yet, as the SPAC ecosystem matures, the limitations of warrants are becoming increasingly evident, prompting a case for adopting rights-based unit structures, with 45 out of 145 searching SPACs adopting a rights-only structure. We discuss below the limitations of the warrants-based structure and the advantages offered by the rights-based unit structure adopted by HVII.

- A primary issue with warrants is their misunderstanding and subsequent mispricing in the market. Warrants are complex derivatives, influenced by factors like volatility, time to expiry, and strike price, making their true value difficult for many retail and even institutional investors to ascertain. This often leads to inefficient pricing, where warrants trade at either a premium or discount to their theoretical value, creating arbitrage opportunities for sophisticated players but potentially eroding value for less informed participants.

− Second, warrants create significant valuation headaches for both the SPAC sponsor and the target company post-merger. For SPACs, accurately valuing warrants for financial reporting (e.g., ASC 815 or IFRS 9) requires complex models and assumptions, leading to volatile earnings. Post-merger, the newly public target company inherits this complexity. The fluctuating value of warrants on their balance sheet can obscure underlying operational performance and introduce volatility to reported financials and the company’s ability to forecast earnings, complicating investor relations and analysis.

− Finally, warrants perpetuate an overhang on the common shares post-merger. The existence of a large pool of outstanding warrants, exercisable at a set price, represents potential future dilution. As the common stock price rises above the warrant strike price, warrant holders are incentivized to exercise, increasing the number of shares outstanding. This continuous overhang of dilution can cap the upside potential of the common shares and create selling pressure, hindering post-merger stock performance.

− By contrast, the rights-based unit structure adopted by HVII offers a more streamlined, transparent, and investor-friendly alternative. One of HVII’s standout features is its zero-warrant structure paired with a simple 1/12th right per unit. Rights, which grant the holder the ability to receive a fraction of an additional share upon merger, are typically less complex and have a shorter lifespan than warrants. This inherent simplicity reduces the potential for mispricing, simplifies valuation for financial reporting, and largely eliminates the long-term overhang on common shares, as rights are either exercised or expire relatively quickly after the de-SPAC transaction.

• For target companies, this eliminates the complexity and potential dilution risk that often comes with SPAC warrants, which can weigh on the share price and complicate future fundraising. As market participants seek structures better aligned with sustainable value creation, rights-based SPACs like HVII are emerging as a new standard in an evolving market as they enhance transparency and position the combined company for healthier post-merger stock performance.

Chart 10: Structure of SPACs Actively Searching for a Target

- Performance-based fees enable lower cost, aligned interests. Target companies often worry about excessive SPAC-related costs draining precious capital. HVII addresses this by negotiating significantly reduced, performancebased underwriting fees with its lead underwriters at Cohen Capital Markets. This means that the bulk of fees are paid only when value is delivered. This structure ensures that more cash is available for the business’s operational needs post-merger, such as scaling production, investing in technology, or expanding into new markets. For potential merger partners, this provides confidence that HVII’s team and underwriters are aligned in creating long-term value, not just closing a transaction for short-term gain.

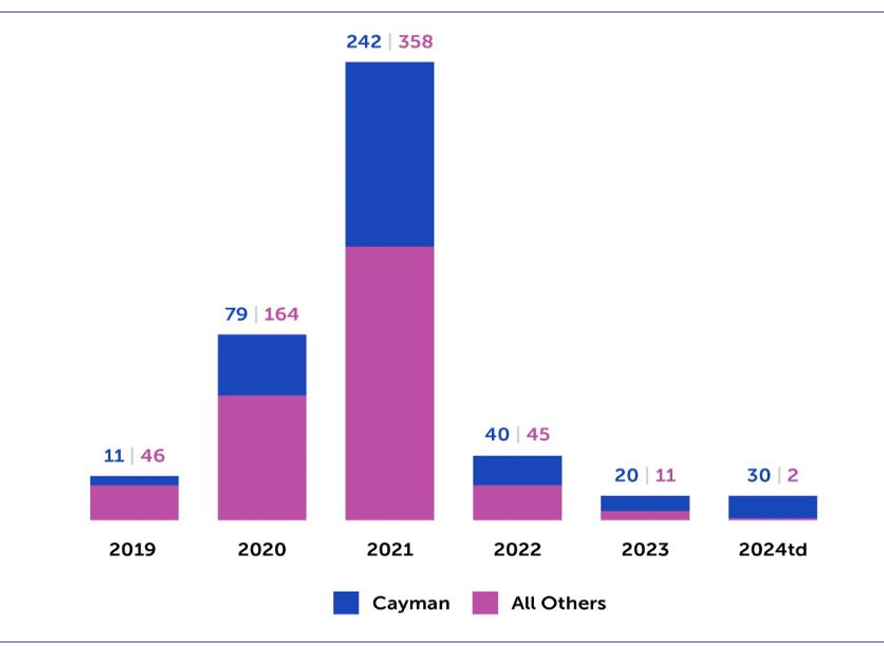

- Cayman domicile advantage results in efficient cross-border deal execution. HVII’s Cayman Islands domicile offers important advantages for target companies, particularly those in industrial technology and energy transition sectors that may have international operations. The Cayman structure helps minimize tax friction and regulatory complexities during the merger process, compared to Delaware SPACs that can trigger additional approvals and costs. For target companies, this means a faster, more predictable path to closing, and fewer distractions from executing on strategic goals.

Chart 11: Cayman Islands Has Become a Preferred SPAC Domicile Location

- Track record of navigating compliance for a smooth listing. Navigating SEC and Nasdaq regulations is one of the most critical and complex parts of going public via SPAC. HVII’s leadership team brings extensive experience in structuring deals that meet the highest regulatory standards. This proactive, disciplined approach helps reduce execution risk for target companies, ensuring that the merger process is not derailed by avoidable compliance issues. For potential partners, this means greater certainty of closing and a stronger foundation for success as a public company.

Fundamentals & Risk Factors

Balance Sheet Snapshot

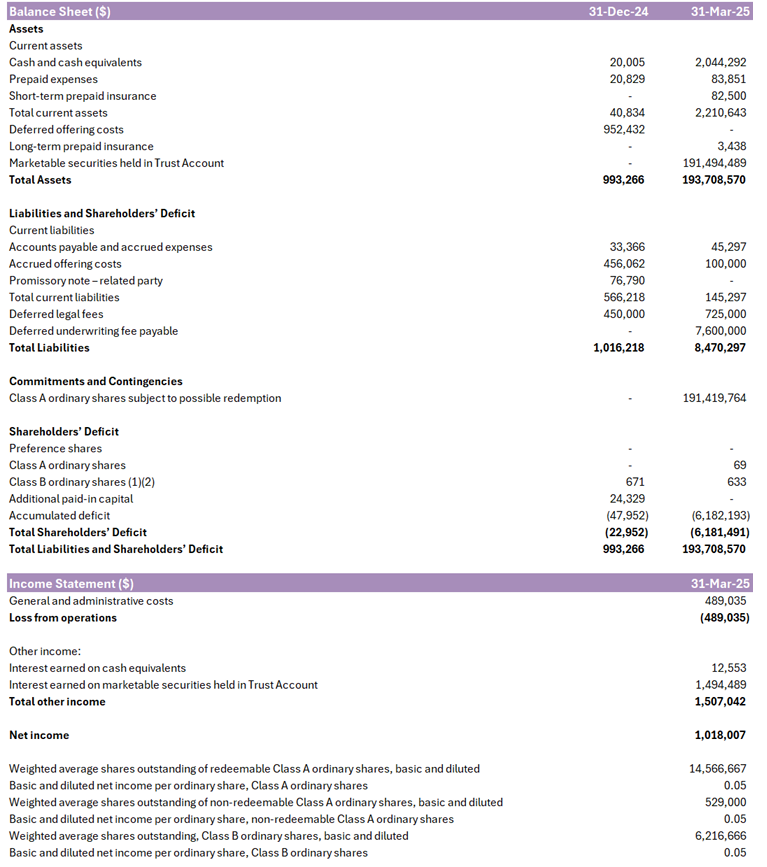

- As of 1Q25, the assets held in HVII’s Trust Account amounted to $191.4 million and the company had cash and cash equivalents of ~$2 million. The company’s Business Combination must be with one or more target businesses that together have a fair market value equal to at least 80% of the net balance in the Trust Account (excluding the amount of deferred underwriting discounts held and taxes payable on the income earned on the Trust Account) at the time of the signing an agreement to enter into a Business Combination. HVII generates non-operating income in the form of interest income on investments from the proceeds derived from the IPO.

Chart 12: HVII – Financial Snapshot (as of March 31, 2025)

Risk Factors

- Regulatory uncertainties: HVII may face significant regulatory challenges when attempting to complete a business combination, particularly if the target company is based in the U.S. and the transaction involves any foreign influence. U.S. government entities, such as the Committee on Foreign Investment in the United States (CFIUS), have the authority to review or block deals that pose national security concerns. Even if the sponsor is a U.S.-based entity with no substantial foreign ties, CFIUS has broad jurisdiction, especially under recent legislation that allows reviews of minority investments linked to critical infrastructure, technologies, or sensitive personal data. This regulatory scrutiny can delay or restrict business combinations, reduce the pool of eligible targets, and place HVII at a competitive disadvantage compared to SPACs without such perceived risks.

- Changes in international trade policies, tariffs and treaties. Tariffs, or the threat of tariffs or increased tariffs, could have a significant negative impact on certain businesses (either due to domestic businesses reliance on imported goods or dependence on access to foreign markets, or foreign businesses’ reliance on sales into the U.S.). In addition, retaliatory tariffs could have a significant negative impact on foreign businesses that rely on imports from the U.S., and domestic businesses that rely on exporting goods internationally. These tariffs and threats of tariffs and other potential trade policy changes could negatively affect the attractiveness of certain business combination targets, or lead to material adverse effects on a post-business combination company.

- Redemption timing: If HVII fails to complete a business combination within 24 months of its IPO, public shareholders may face delays in receiving their funds. Although the company is required to redeem public shares using the trust account proceeds—including any interest earned—this redemption is only triggered automatically upon liquidation. Until that point, shareholders have no right to early access unless a combination is completed or the charter is amended to allow early redemption. In the event of liquidation, the process must comply with Cayman Islands law and may take additional time, potentially extending the wait period for investors. As a result, shareholders could experience an unexpected delay in retrieving their capital, even beyond the original 24-month deadline.

- Competition: HVII operates in a highly competitive environment where many firms including experienced private investors and rival SPACs, are also seeking promising acquisition targets. These competitors often possess deeper financial reserves, larger networks, and greater industry knowledge, giving them a natural advantage in sourcing and closing deals. As HVII must commit to redeeming public shares in cash during a business combination, potential targets may perceive limited available capital, reducing the company’s appeal. This constraint becomes particularly relevant when bidding for larger businesses, where financial capacity can influence deal success. Despite a wide range of possible targets, HVII’s ability to win competitive bids may be constrained by both external rival strength and internal redemption-related cash reductions.

- Post-merger financial risks: After completing a business combination, HVII may face unexpected financial setbacks such as asset write-downs, impairments, or restructuring charges. These issues can arise even after thorough due diligence, as not all material risks may be visible beforehand or within HVII’s control. Such charges, while possibly non-cash, can negatively impact financial results, harm investor confidence, and reduce the market value of the company’s shares. In certain cases, these accounting losses may also cause breaches in financial covenants tied to existing or newly assumed debt. As a result, investors choosing to hold shares after the merger could see diminished value in their holdings, especially if market sentiment turns cautious due to reported losses or operational disruptions.

- Financing uncertainty: HVII may need additional capital to complete or grow a target business post-merger, especially if the chosen target exceeds the size of its available funds. There is no guarantee that financing will be available on acceptable terms, or at all. If HVII cannot raise the required funds, it may be forced to restructure or abandon a potential deal. Financing needs may increase due to redemptions, operational requirements, or negotiated terms. Failure to secure funding could disrupt a merger or slow the growth of the acquired company. If no business combination occurs, shareholders may receive only ~$10 per share, and Share Rights will expire worthless.

- Dilution from founder shares: HVII’s sponsor acquired founder shares at a nominal cost of $25,000, or just ~$0.004 per share. In contrast, public investors buy in at $10.00 per unit. Upon completion of a business combination, these founder shares convert into Class A ordinary shares, which may significantly dilute the value of public shares. For instance, assuming an equity value of $168 million and no redemptions, each share could be valued at $7.00 postmerger 30% below the initial public offering price. This dilution results purely from the low-cost basis of the founder shares, not taking into account other expenses or market conditions.

.jpg)

Contact Us